{kind=link}

July’s auto gross sales noticed plugin EVs take 24.0% share in France, up from 20.8% year-on-year. BEVs grew share, while PHEV remained flat. General auto quantity was 116,350 items, down some 8% YoY. The Renault 5 was the best-selling BEV for the month.

July’s auto gross sales totals noticed mixed plugin EVs take 24.0% share in France, with 16.8% full battery-electrics (BEVs) and seven.2% plugin hybrids (PHEVs). These examine with YoY figures of 20.8% mixed, 13.5% BEV, and seven.3% PHEV.

The year-on-year baseline comparability was skewed by a sluggish interval in 2024 between the top of recent “social leasing” signings and the arrival of the Citroen e-C3 and the Renault 5 within the Autumn. So, while the YoY uptick seems optimistic, the baseline was in reality abnormally low. Extra usually, the plugin market share has barely risen since late 2023, because the beneath powertrain timeline graph clearly exhibits.

The extra notable development has been the alternative of ICE-only gross sales with non-plugin hybrids (HEVs and MHEVs), represented by the quickly rising blue section within the graph beneath. This demonstrates that legacy auto firms are usually taking a “lowest hanging fruit” strategy to assembly emissions necessities, fairly than going all in on plugins, and particularly on BEVs.

Nonetheless, with extra inexpensive BEVs like the brand new Renault 5 and Citroen e-C3 usually seeing sturdy volumes lately, and the Hyundai Inster debuting in July, with the BYD Dolphin Surf about to make first buyer deliveries, plugin share might quickly enhance in France.

Finest Promoting BEV Fashions

The Renault 5 was as soon as once more one of the best promoting BEV in July, with 2,033 items, its fourth time within the high spot this 12 months (and by no means out of the highest two). In second place was the BMW iX1, with a private finest 1,084 items. In third was the Tesla Mannequin Y, with 979 items.

July volumes had been pretty weak general, with the BMW iX1 being the one member of the highest 10 seeing progress over latest averages – thus its sturdy ascent to second place. Nevertheless, that is a longtime seasonal sample, with July and August usually the slowest months of the French auto market.

Additional again, the brand new Renault 4 maintained its twelfth place from June, and might absolutely climb increased.

There was one vital debutant in July, the brand new Hyundai Inster, which landed in seventeenth place, with 336 preliminary items. There’s each cause to count on the Inster to shortly climb to over 500 items per 30 days and begin competing with the home small-and-affordable competitors.

We don’t but have visibility on what’s occurring with the brand new BYD Dolphin Surf in France, past the beneficiant 414 showroom items which arrived in Could. The Surf is already promoting a whole lot of month-to-month items in every of the massive neighbouring markets of Germany, Italy, Spain (the place it ranked 2nd in July), and the UK. Let’s be careful for its transfer to buyer deliveries in France.

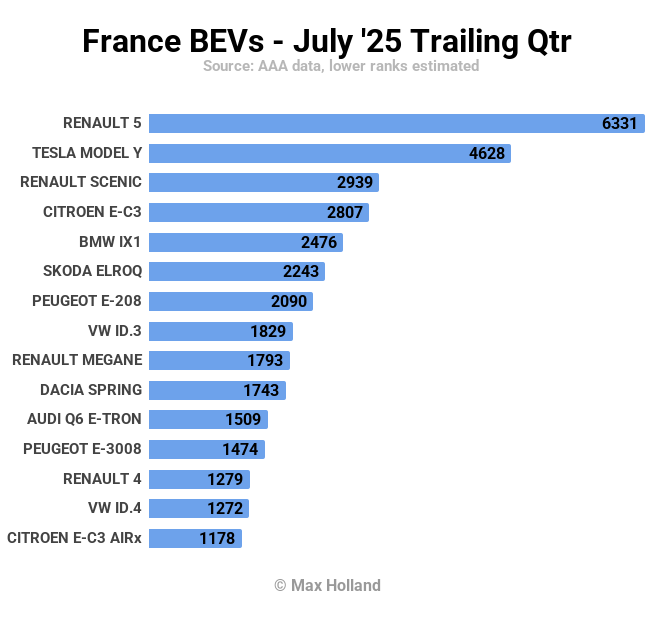

There’s no nice shock in regards to the high two spots within the trailing 3-month rankings. The Renault 5 is in fact main, with 6,331 items. After a powerful June, the Tesla Mannequin Y (with 4,628 items) is safely in second place, effectively forward of the third positioned Renault Scenic (2,939 items).

The Renault 4 is now firmly within the mid-rankings (thirteenth), and we are able to count on it to enter the highest 10 sooner or later, as soon as manufacturing quantity is ramped. The Citroen e-C3 Aircross continues to be seen solely by advantage of its sturdy Could, having seen a lot weaker volumes in June and July.

How lengthy earlier than the Hyundai Inster makes it into the above chart? I might guess maybe someday in This fall.

Outlook

July was the fifteenth consecutive month of falling YoY quantity within the French auto market, with December 2024 being the one exception (and even that was successfully flat YoY).

The broader macroeconomy is in step with this development, with newest Q2 2025 information displaying 0.7% YoY GDP progresssustaining the weak spot seen in Q1, and This fall 2024.

Headline inflation was regular at 1% in July (from a revised-up 1% in June). ECB rates of interest have remained at 2.15% since early June. Manufacturing PMI barely shifted, at 48.2 factors in July, from 48.1 factors in June.

What’s subsequent for the French auto market? When may we see BEV progress resume? What BEV fashions are wanted and at what value factors? Please bounce in beneath along with your ideas and views, and be part of the dialog.

Join CleanTechnica’s Weekly Substack for Zach and Scott’s in-depth analyses and excessive degree summariesjoin our each day e-newsletterand comply with us on Google Information!

Have a tip for CleanTechnica? Need to promote? Need to recommend a visitor for our CleanTech Discuss podcast? Contact us right here.

Join our each day e-newsletter for 15 new cleantech tales a day. Or join our weekly one on high tales of the week if each day is simply too frequent.

CleanTechnica makes use of affiliate hyperlinks. See our coverage right here.

CleanTechnica’s Remark Coverage

Valvoline Advanced Full Synthetic SAE 0W-20 Motor Oil 5 QT

$26.97 (as of February 24, 2026 23:22 GMT -08:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Amazon Basics Microfiber Cleaning Cloths, Ultra Absorbent, Lint Free, Streak Free, Non-Abrasive, Reusable and Washable, 16" x 12", Blue/White/Yellow, Pack of 24

$9.98 (as of February 24, 2026 23:22 GMT -08:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Rain-X 810363 Repellency Water Repellent Wiper Blades, 22" Windshield Wipers (Pack of 2) New & Improved Version of Latitude [Amazon Exclusive]

$31.96 (as of February 24, 2026 23:22 GMT -08:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Rain-X 600001 Windshield Repair Kit - Quick and Easy Durable Resin Based Windshield Repair Kit for Chips and Cracks, Good for Round Damage Below 1" in Diameter and Cracks Smaller Than 12" in Length

$10.99 (as of February 24, 2026 23:22 GMT -08:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Rain-X 820149 WeatherBeater Wiper Blades, 22" Windshield Wipers (Pack of 2), Automotive Replacement Windshield Wiper Blades That Meet Or Exceed OEM Quality And Durability

$26.88 (as of February 24, 2026 23:22 GMT -08:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

GOOACC 240PCS Bumper Retainer Clips Car Plastic Rivets Fasteners Push Retainer Kit 12 Popular Sizes Auto Push Pin Rivets Set -Door Trim Panel Fender Clips for GM Ford Toyota Honda Chrysler

$15.08 (as of February 24, 2026 23:22 GMT -08:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Loctite Threadlocker Blue 242 - Removable Thread Lock Glue for Nuts, Bolts, & Fasteners, Medium Strength Screw Glue to Prevent Loosening & Corrosion - 6 ml, 1 Pack

$5.93 (as of February 24, 2026 23:22 GMT -08:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)