{kind=link}

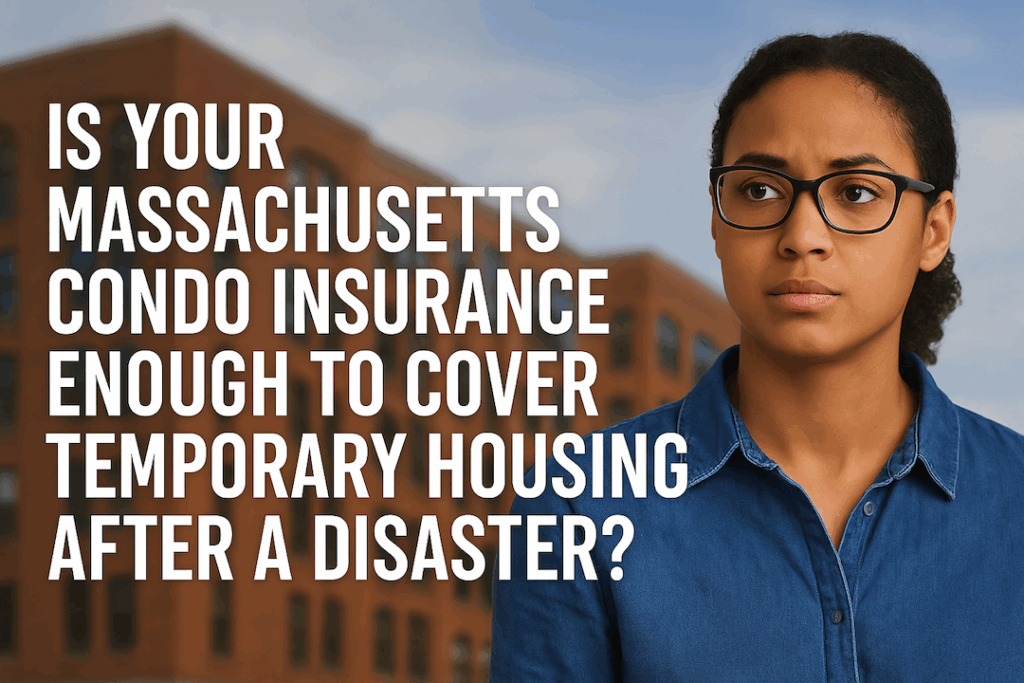

What occurs in case your rental turns into uninhabitable after a fireplace or water loss?

Would your present insurance coverage coverage cowl the price of a short lived place to reside?

? Understanding Lack of Use in Your HO6 Condominium Insurance coverage Coverage

? How Is Lack of Use Protection Calculated?

?? However Is That Sufficient to Cowl Your Non permanent Residing Bills?

? Your Condominium Affiliation’s Grasp Coverage Doesn’t Cowl This

? What You Can Do Proper Now: Evaluate and Modify Your Protection

? Remaining Ideas

SINGARO Car Cup Holder Coaster, Silicone Cup Holder Insert, Universal Non-Slip Cup Holders, Car Accessories Interior for Women and Man Interior Sets 4 Pack Black

$6.99 (as of February 24, 2026 23:22 GMT -08:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Mobil 1 Extended Performance Full Synthetic Motor Oil 0W-20, 5 Quart

$29.97 (as of February 24, 2026 23:22 GMT -08:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

AUTOBOO 26" and 16" Windshield Wipers Blades (Pack Of 2),OEM Quality Premium All-Seasons Wiper blades,Stable and Quiet Armor wiper blades

$16.99 (as of February 24, 2026 23:22 GMT -08:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

USANOOKS Microfiber Cleaning Cloth Grey - 12 Pcs (12.5"x12.5") - High Performance - 1200 Washes, Ultra Absorbent Microfiber Towel Weave Grime & Liquid for Streak-Free Mirror Shine - Car Washing Cloth

$6.98 (as of February 24, 2026 23:22 GMT -08:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Amooca Car Seat Headrest Hook 4 Pack Hanger Storage Organizer Universal for Handbag Purse Coat fit Universal Vehicle Car Black S Type

$6.99 (as of February 24, 2026 23:22 GMT -08:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

Kaistyle for Magsafe Car Mount【20 Strong Magnets】Magnetic Phone Holder for Car Phone Holder Mount Dash Mounted Holders Cell Phone Holders for Your Car Accessories for Women Men for iPhone 17 16 15 14

$9.98 (as of February 24, 2026 23:22 GMT -08:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)

NOCO Boost GB40: 1000A UltraSafe Jump Starter – 12V Lithium Battery Booster Pack, Portable Jump Box, Power Bank & Jumper Cables - for 6.0L Gas and 3.0L Diesel Engines

$99.95 (as of February 24, 2026 23:22 GMT -08:00 - More infoProduct prices and availability are accurate as of the date/time indicated and are subject to change. Any price and availability information displayed on [relevant Amazon Site(s), as applicable] at the time of purchase will apply to the purchase of this product.)